Owning a home in the USA is less about the house itself and more about taking on debt advantageously (i.e. someone else owns it).

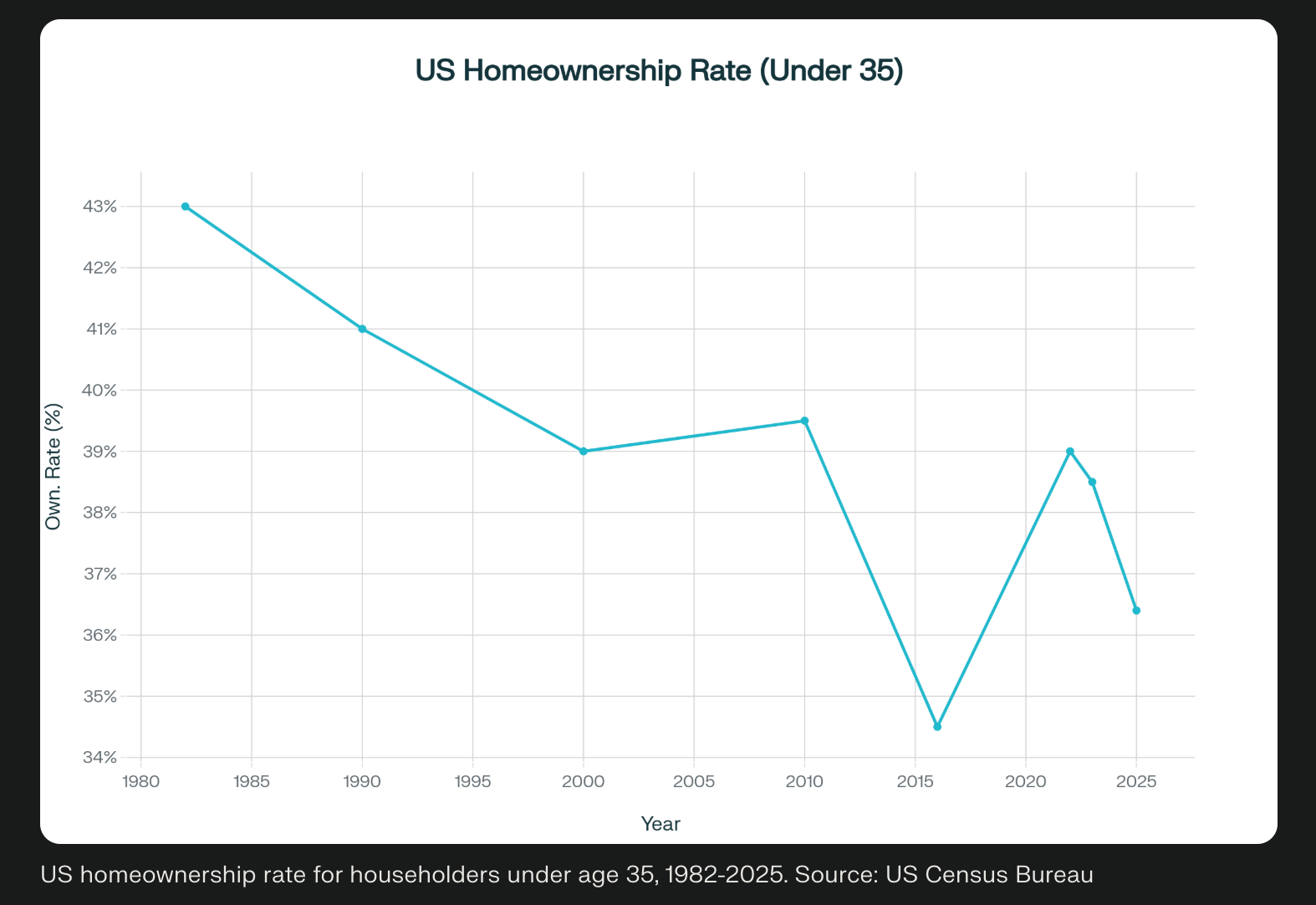

Another Eisenhower-era boom in home ownership?

Owning a home … the American Dream! but for who? While it remains a trope for familial permanence, a home at its core is a financial instrument embedded in a dense ecosystem of tax rules, credit and equity markets, and social expectations.

Only the USA and Denmark offer 30-year fixed rate mortgages; unsurprisngly a 50‑year mortgage elicits moral and existential reactions.

“People will be indebted for life.”

Rather than use the words: good or bad, Let’s reframe debt as “the point” of home ownership. Specifically, the functional utility of mortgage‑based leverage.

Mortgages are a way to convert future income into current purchasing power.

Refinancing, in particular, allows us to take out equity from our home. That means if you previously put 20% down (150K) on your $750,000 house, when you refinance the lender will give you your 150K back (probably more) AND your interest rate will decrease.

And the 150K they give back to you is not taxable income.

Do you ever wonder why Jay-Z and Beyonce have 90,000+ square feet of home spread across the country?

The “payout” is tax-free because the lender is reconfiguring the terms of the debt relationship. Don’t listen to people saying “it’s a scam”.

It’s just the way it works

It’s up to you to remain ignorant or make the system work for you.

As I have covered here and here and here the US Dollar is the world’s reserve currency and access to tax-efficient liquidity is America’s gift to its citizens.

Savvy homeowners and investors use debt and re-fis to accumulate further assets. From 1031-Exchanges to Delaware Statutory Trusts, financial products exist specifically to let property owners recycle equity into new investments.

Risky Business

Hypothetically extending the repayment window from 30 to 50 years increases the length of exposure to interest rate risk and may shift incentives for maintenance, mobility, and intergenerational wealth transfer. Not every household benefits equally.

People with unstable incomes or weak financial literacy will suffer. Many ideas are plainly bad. And then there are ideas with pros and cons that must be balanced against context and the incentives they create. The 50-year mortgage is one of these ideas.

At the macro level, lengthening mortgage horizons (i.e. more leverage) gives the USA a perfect wrapper to print more dollars, which creates additional credit capacity, which enables asset purchases. We now know the SLR threshold will go down for the GSIBs. And demand for dollars will now be recycled via global citizens due to USD-denominated Stablecoins.

If the administration pulls this off; there will be overflowing capital to fund everything from residential investment to broader economic initiatives. As we stand on the brink of enormous capital needs; specifically upgrading up-stream energy production and down-stream energy distribution while deploying AI infrastructure, the prospect of more low‑cost, long‑duration credit into productive projects is strategically significant.

Remember

My point here is not to make moral judgments on whether this is good or bad. The point is to make the economic system work for you depending on choices that are made outside of your control. There are plenty of ways on this Earth to support and promote fellow humans. Our ability to do so increases the more able we are to achieve financial independence.

Your mortgage rate should function as your hurdle rate: if you can deploy capital at returns above your mortgage interest, then you can benefit by increasing your debt prudently. A longer term mortgage often lowers monthly burden or changes the structure of payments, enabling borrowers to allocate capital toward higher‑return opportunities.

This 🤖 is not financial advice 🤖 nor an argument to encourage reckless behavior.

It’s an argument to treat your home as a deliberate tool within a broader portfolio strategy.

Like any powerful tool (did I hear someone say AI?), extended‑term mortgages would create winners and losers. The question isn’t: should we be free of debt forever? - it’s whether we use debt to productively multiply opportunity across society.

If you are worried about “getting out of debt” you should not own a home.

The whole point of homeownership is to get into debt.

Click the button below to dive deeper into this essay.