Holistic Finance

wtf is it? 🤷🏽♂️

I am not sure. But I was asked to give a talk about it … so I’ll be fakin’ it ‘till I make it like everyone else.

So far this is where I’ve got to: HF might be about integrating personal, business, and macroeconomic perspectives.

And I think feel “holistic” might matter in a world of siloed financial advice.

Everyone has an agenda, which means YOU need one too.

Here are some topics that I think are important. Let me know what you think. What resonates? What else might be important to learn?

I. Time Value of Money

Money today is worth more than money tomorrow.

Simply put if someone owes you $100 - it is more valuable to you if they pay you back today. That $100 will be worth less one year from now.

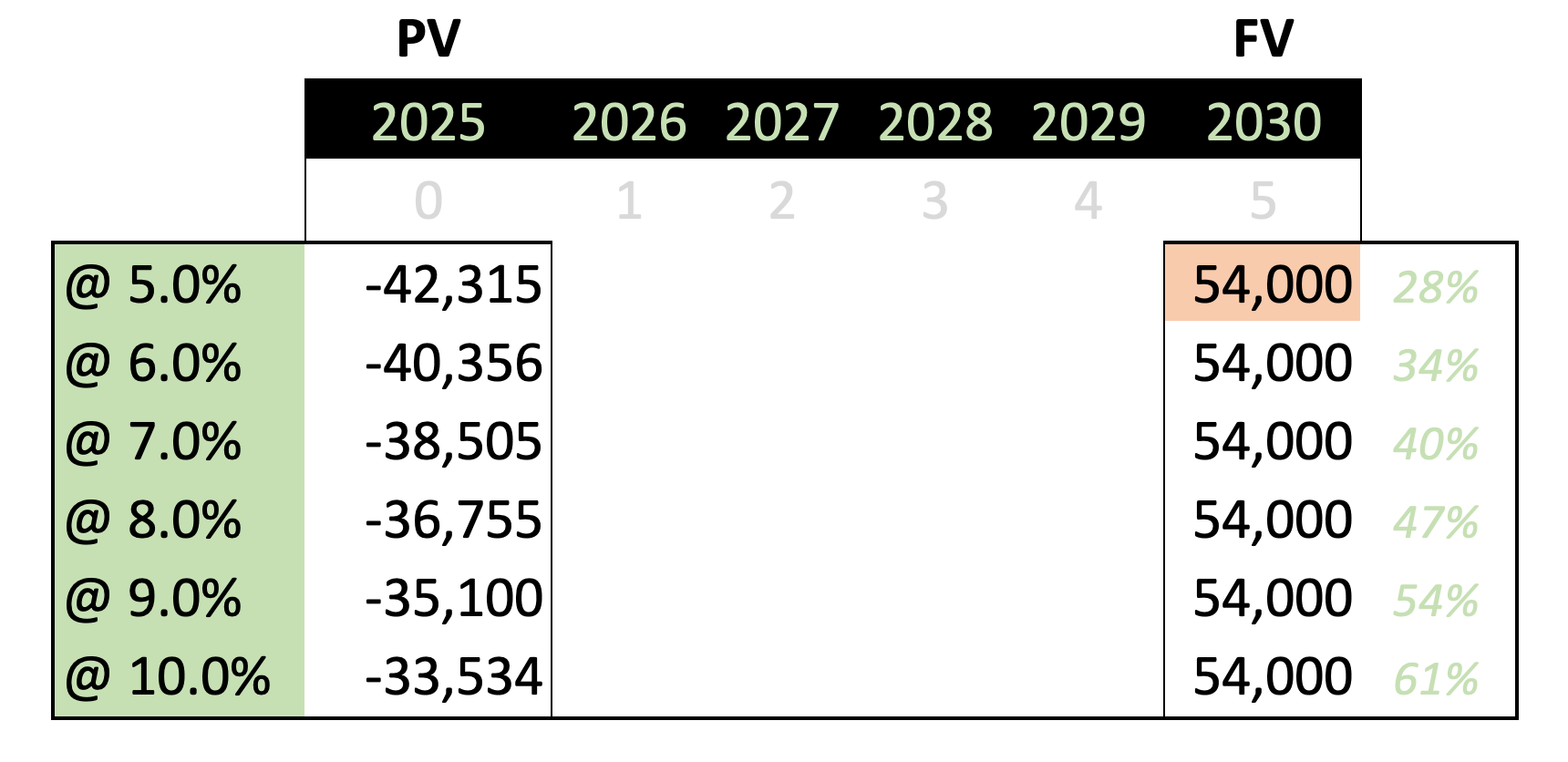

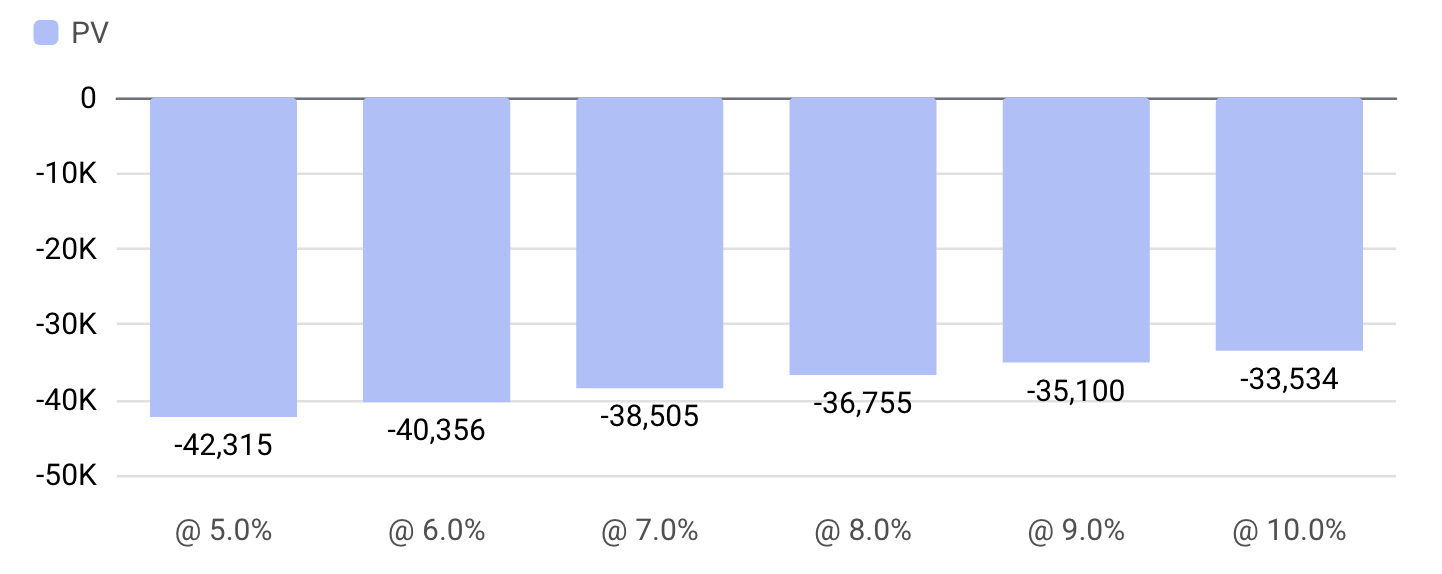

Present Value is an instrumental concept to grasp when saving for the future as well. Let’s assume your plan is to save money for a downpayment on a house in five years.

If you can earn 5% yield on your money then you will have 54K by 2030 if you invest just over 42K today.

If you are one of the lucky ones who has access to preferential investment opportunities you might be able to earn 10% on your funds. And if so then you can invest only 33.5K today and still end up with 54K in five years.

That’s the time value of money; hopefully this example conveys the power of compounding and why patience is a superpower in finance.

Try the Future Value Calculator here

II. Setting Goals & Managing Expenses

The top line is often unpredictable …

If you are on a salary there is always a risk that you might lose your job and if you are a founder your “hopes and prayers” may not be answered in the form of revenue.

Hence below the line aka expense management is your only real precision lever. And of course we can’t always predict costs, especially when emergencies strike.

It’s imperative to know your burn rate and how it dictates your survival.

To calculate your runway, assume you have no income and then figure out how many months of expenses you can cover with no money coming in the door.

The goal is to always have more runway.

III. Allocation, Diversification, and Risk

Allocation, allocation and allocation.

We are inundated with recommendations on where to invest, how much to allocate between stocks and bonds, and why diversification is important.

Yet diversification is not an end in itself. In fact, there are risks of both over- or under-diversifying.

Concentrating your investment allocation can be a risk, however did you know it is the preferred strategy for most successful money managers who control proprietary capital?

Your investment strategy should assess and mitigate risk that is specific to you. A 60/40 portfolio is primarily a consensus marketing mechanism rather than a framework for generating alpha.

IV. Inflation

I’ve written about inflation here, here, here and here.

I like talking about it because we as a society don’t understand how it works. Even worse the concept is simply mis-taught. The de facto economics we learn is Keynesian (it’s been the prevailing system during our lifetimes) and Classical (the system before that). Most people know far less if anything at all about the Austrian School (the system before that).

When you go back far enough you realize that people must share the same economic value system to truly get along.

So inflation plays a major role in how each of these systems think about labor, customers, value and intervention.

It’s important for YOU to determine your personal rate of inflation. It is the only thing that matters.

Everyone’s inflation is different; it depends on your “basket” (education, housing, healthcare, etc.).

Challenge:

Calculate your own personal inflation rate and observe how it impacts goal-setting.

If you’re not beating your personal inflation rate, you’re falling behind; even if the headlines say inflation is low.

Recap:

I. Money Has Time Value

II. Manage Expenses

III. Allocate To Mitigate Risk

IV. Personal Rate of Inflation